Card Features and Security Elements

Card features and security elements are integral components that ensure the safety and functionality of payment cards. The card issuer and card number are fundamental attributes that identify the financial institution and the specific account associated with the card. Cardholder information, such as the name and potentially other personal details, further personalizes the card. The valid thru date and credit card hologram are additional security measures that help validate the card’s authenticity and the cardholder’s identity.

The EMV chip and magnetic stripe are crucial for storing and transmitting data during transactions, offering enhanced card security against fraud. The expiration date, hologram, and signature panel are additional security measures that help validate the card’s authenticity and the cardholder’s identity. Smart cards, equipped with integrated circuits, provide advanced capabilities for secure data storage and processing.

The significance of card features and security elements lies in their ability to protect against unauthorized access and fraudulent activities. Card features and security elements ensure that transactions are conducted securely, maintaining the integrity of the payment system. The EMV chip, in particular, has been instrumental in reducing counterfeit card fraud by generating unique transaction codes that are unable to be reused. The magnetic stripe, although less secure than the chip, remains in use for backward compatibility. The hologram and signature panel serve as visual card security features that merchants quickly check to verify the card’s legitimacy.

The major cards accepted in most transactions worldwide include Visa, MasterCard, Discover, and American Express. Visa, MasterCard, Discover, and American Express are recognized for their global acceptance and the comprehensive security features they offer. Visa and MasterCard, with their vast network, are particularly prevalent in international transactions. Discover and American Express are known for their rewards programs, customer service, and card security measures.

Protecting a card involves several practices to safeguard it from theft, loss, and unauthorized use. Regularly monitoring transaction statements, using strong passwords for online accounts, and enabling transaction alerts are effective ways to detect and respond to suspicious activity. Keep the physical card secure, cover the CVV when entering it online, and be cautious when using it in public places or on unsecured networks.

Amplify is a platform dedicated to secure giving, which incorporates robust security measures to ensure the safety of donations and personal information. Amplify provides a trustworthy environment for charitable transactions by leveraging encryption, secure payment gateways, and compliance with industry standards. The platform’s focus on security protects donors and reinforces the credibility of the organizations it supports, fostering a culture of safe and reliable giving.

1. Card issuer

The card issuer plays a crucial role in financial transactions, often including banks or financial organizations that provide credit or debit cards to clients. The card issuer is authorized to establish the terms and conditions associated with the card, including credit limits and interest rates, and assumes the duty of protecting the card’s authenticity and preventing fraudulent behavior.

The card issuer is not physically accessible on the card itself but is identified by the emblem, or name affixed to the card’s surface regarding the geographical aspect, which serves as an indication of the institution supporting the card. The card issuer’s responsibility goes beyond simple distribution; it serves as the mediator in financial transactions, granting authorization and processing payments, and safeguarding the cardholder’s information.

The card issuer deemed praiseworthy or reputable is distinguished by its robust security protocols, clear contractual conditions, and prompt customer support, all of which enhance the security and user-friendliness of the cardholder’s experience. An unscrupulous entity or a deceptive one demonstrates indications of inadequate security measures, ambiguous conditions, or uncooperative assistance, posing a potential threat to the financial well-being of the cardholder.

The card issuer is immensely important since it is the basis for the cardholder’s financial activities. A reliable issuer enables smooth transactions and fosters trust in the cardholder, guaranteeing the security of their financial assets.

2. Card number

The card number, often known as the primary account number (PAN), is a unique sequence of numbers that is engraved or written on the card. The function of the card number is twofold: it acts as the identifier for the card issuer and the cardholder’s account, and it plays a vital part in transaction processing.

The card number is on the face of the card, commonly the visa first 4 digits. The card’s most notable characteristic is its prominent placement, facilitating convenient access for cardholders and merchants during transactions.

The card number plays a crucial role in facilitating the transaction process in addition to its primary purpose of identification. Using the card number at the initiation of a transaction serves the purpose of directing the payment from the cardholder’s account to the merchant account, guaranteeing an accurate cash transfer.

A good card number is a legitimate numerical identifier that aligns with an active account with enough assets or credit. A bad card number pertains to an invalid, an expired, or a number linked to a closed or overdrawn account, resulting in negative transaction outcomes.

The card number is important since it is the fundamental support for electronic payment systems. The fundamental component facilitating the smooth implementation of financial transactions is the important factor, allowing cardholders to make purchases and payments conveniently and effectively.

3. Cardholder information

The cardholder information is an essential element in financial transactions, including using credit or debit cards. The cardholder’s name is the main component, either embossed or written on the front of the card. It includes supplementary information such as the billing address. The data is often stored on the tangible card and saved in the card issuer’s database.

The cardholder information primarily authenticates the cardholder’s identity, especially in online or phone transactions when the actual card is absent. Merchants and financial institutions enhance the credibility of transactions and mitigate the potential for fraudulent activity by cross-referencing the cardholder information given during the transaction with the data maintained by the card issuer.

An exemplary illustration of the use of cardholder information is its successful implementation in mitigating unlawful transactions, guaranteeing that only the authorized cardholder has the ability to begin and complete a transaction. An unfavorable use scenario includes inadequate verification procedures, increasing vulnerability to fraudulent activities, and identity theft.

Cardholder information is crucial for ensuring the security and integrity of financial transactions, making it of utmost significance. It functions as a first barrier against fraudulent activities and plays an essential role in safeguarding the cardholder’s financial resources and the trustworthiness of the payment system.

4. EMV chip

The EMV chip, which stands for Europay, Mastercard, and Visa, is a sophisticated security mechanism included in contemporary credit and debit cards. The little, metallic square is often positioned on the front of the card, near the cardholder’s name, or over the card number. The EMV chip’s unique look distinguishes it from the rest of the card’s surface, making it readily identifiable.

The principal purpose of the EMV chip is to augment the card security of card transactions, especially in situations involving direct interpersonal interaction. The EMV chip produces a distinct, singular code for every transaction, substantially reducing the potential for fraudulent activities with counterfeit cards when used in a chip-and-PIN transaction. Implementing the dynamic authentication procedure represents a notable progression compared to the static data stored on conventional magnetic stripes, which is susceptible to greater ease of replication or duplication.

An exemplary illustration of the use of EMV chips is seen inside a retail environment, wherein chip-enabled point-of-sale (POS) terminals are employed. The chip guarantees the authentication of every transaction under such circumstances, enhancing the security measures for the cardholder and the merchant. An illustrative instance is when a merchant has neglected to enhance their payment terminals to accommodate chip transactions, necessitating the use of the comparatively less secure magnetic stripe, subjecting the cardholder to heightened vulnerability.

The EMV chip has significant relevance due to its capacity to safeguard sensitive cardholder data and mitigate card-present fraud. EMV chips enhance the security of transactions, preserving confidence in the payment system and protecting the interests of customers and financial institutions.

5. Magnetic stripe

The magnetic stripe, sometimes dubbed the magstripe, is a thin band situated on the reverse side of credit and debit cards. A horizontal strip, usually black or brown, is seen on the card, positioned above the signature panel of the cardholder. The magnetic stripe comprises magnetic particles that serve as a medium for storing digital information.

The magnetic stripe is the principal means of storing crucial cardholder data, including the account number, cardholder name, and expiry date. The card is passed via a card reader, retrieving the data stored in the stripe and executing the transaction during a transaction. The magnetic stripe has been the prevailing norm for card transactions for several decades.

Good magnetic stripe use is seen in antiquated point-of-sale (POS) systems, whereby the card is swiftly swiped to commence a transaction. An unfavorable illustration includes only depending on the magnetic stripe for transactions in a setting where card skimming devices are widespread. These devices have the capability to acquire data from the stripe, facilitating illicit transactions and enabling instances of identity theft.

The magnetic stripe is relevant due to its pivotal role in advancing card-based payment systems. A straightforward and efficient method for storing and transmitting cardholder information facilitated the broad acceptance of credit and debit cards. The use of magnetic stripes is diminishing due to their susceptibility to fraudulent activities, owing to the emergence of more robust technology such as the EMV chip.

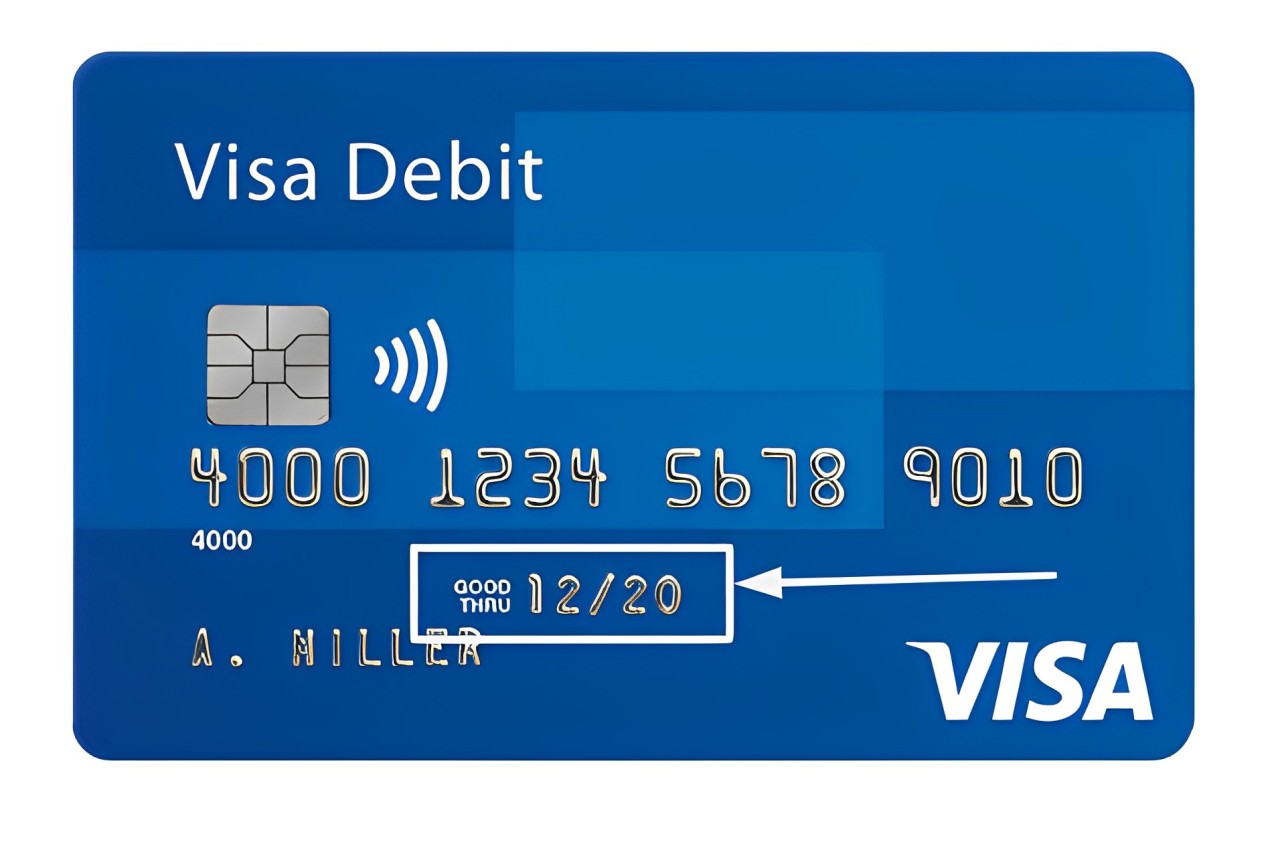

6. Expiration date

The expiration date on a credit or debit card denotes the conclusion of the card’s term of validity, mostly expressed in “good thru” or “valid thru.”. The expiration date is constantly shown on the face of the card, frequently positioned underneath the cardholder’s name or near the card number. The provided date is a month and year (MM/YY), denoting the last month the card is valid for usage.

The expiration date serves as a fundamental security element. Regularly renewing cards helps to minimize the danger of persistent use of lost, stolen, or hacked cards. Issuers incentivize cardholders to update their information and get new cards with enhanced security features by implementing a limited duration for each card.

One good illustration of the expiry date’s purpose is its use within the realm of online transactions, wherein it is often mandated in conjunction with the card number and security code to verify the legitimacy of a payment. A bad instance is when a cardholder persists in using an expired card, oblivious to its invalid condition, resulting in refused transactions and possible annoyance.

The expiration date has significance beyond its function as a security measure. The expiration date functions as a mechanism for card issuers to effectively oversee their card portfolios, guaranteeing their customers’ cards’ continuous currency and security. The expiration date offers a system for the automated elimination of outdated cards that do not possess the most up-to-date security technology or design requirements.

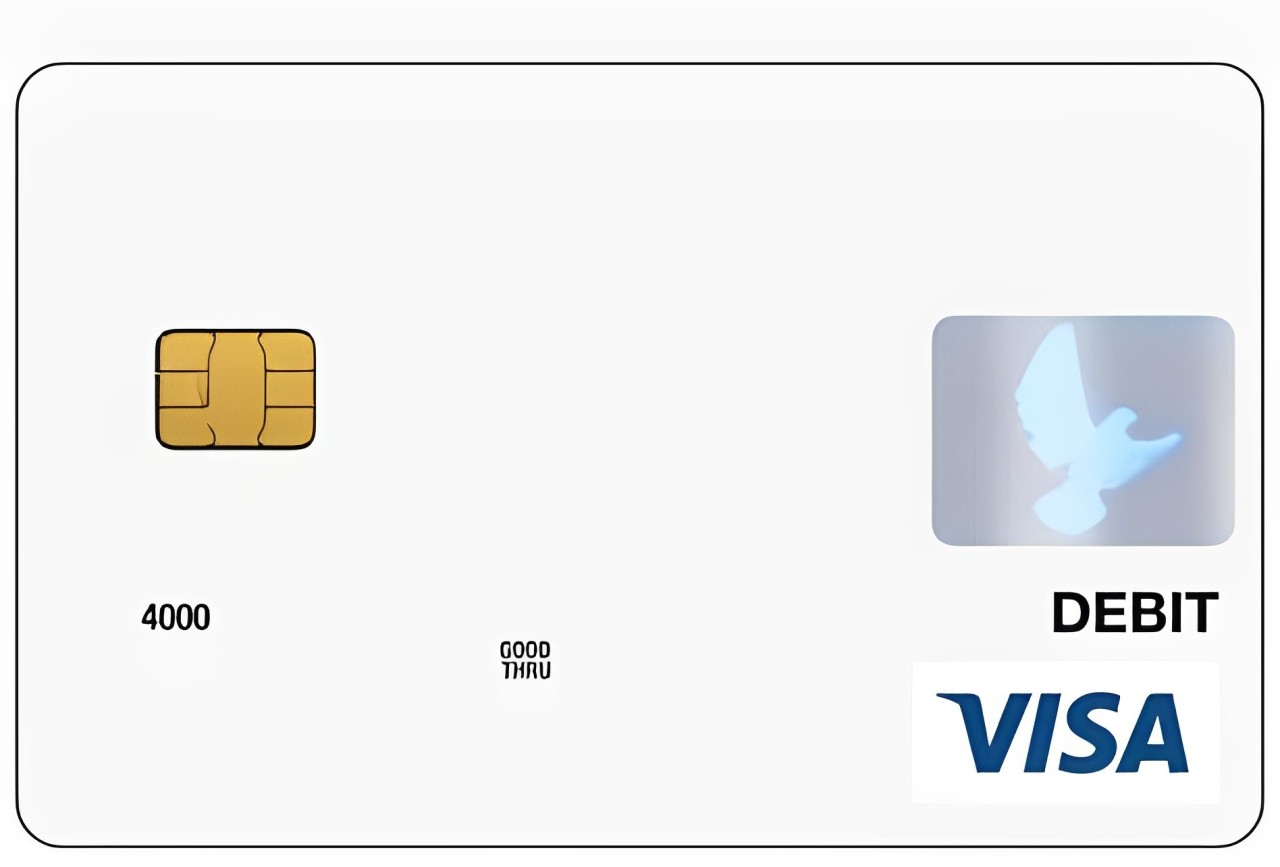

7. Hologram

The hologram on a credit or debit card is a sophisticated security feature typically located on the front of the card, near the card number or the card issuer’s logo. The hologram is a three-dimensional image that appears to shift and change when viewed from different angles, making it a distinctive and easily recognizable feature.

The primary function of the credit card hologram is to serve as a deterrent to counterfeiting. The hologram’s complex structure and the technology required to produce it make it challenging for fraudsters to replicate accurately. The hologram adds a layer of security to the card, helping to prevent the creation and circulation of fake cards.

A good example of the hologram’s effectiveness is its role in the quick visual verification of a card’s authenticity by merchants or during card inspections. A bad example is a poorly designed or positioned hologram that is easily overlooked or does not indicate authenticity, diminishing its security value.

The importance of the hologram lies in its contribution to the overall security of card-based transactions. Holograms help protect cardholders and financial institutions from fraud-related losses by making it more difficult to produce counterfeit cards. Holograms contribute to consumer confidence in the security of their payment instruments.

8. Signature

The signature or signature panel is a designated area on the back of a credit or debit card where the cardholder must sign their name. The signature panel is typically located near the magnetic stripe or at the opposite end of the card. It is usually a white or light-colored space designed to hold an ink signature.

The primary function of the signature panel is to provide a means of verifying the cardholder’s identity. Merchants and financial institutions authenticate the cardholder’s identity and reduce the risk of unauthorized use by comparing the signature on the card with the signature on a transaction receipt or during a card inspection.

A good example of the signature panel’s utility is in situations where the card’s authenticity or the cardholder’s identity is in question. The presence of a matching signature quickly resolves doubts. A bad example is a cardholder failing to sign the panel or using an easily replicable signature, which diminishes the security value of the signature.

The importance of the signature panel lies in its role as a simple yet effective security feature. The signature panel provides a physical, personal identifier to verify the legitimacy of card transactions. The signature panel remains a valuable component of card security, especially in regions or situations where chip technology is not yet prevalent. The reliance on signature verification has decreased with the advent of more advanced security measures such as chip-and-PIN technology.

9. Smart cards

Smart cards are advanced card-based devices with an implanted microprocessor or integrated circuit. Smart cards are generally found within the body of the card, often visible as a small metallic square or contact pad on the card’s surface. The smart card sometimes does not have visible contacts but functions through contactless technology.

The primary function of a smart card is to store and process data securely. The capability allows smart cards to perform various functions, from facilitating secure financial transactions in EMV chip cards to storing loyalty points, personal identification information, and access credentials for secure areas or computer systems. Smart cards execute cryptographic operations, enhancing the security of the data they contain and the transactions they facilitate.

A good example of smart card usage is in the realm of digital security, where they are used to store encryption keys or digital certificates for authentication purposes securely. A bad example is a smart card with insufficient encryption or security features, making it vulnerable to data breaches or unauthorized access.

The significance of smart cards is appreciated in their versatility and the high level of security they provide. Smart cards have become integral to various applications, including financial transactions, identity verification, access control, and data encryption. Smart cards play a crucial role in modern security and data management systems by offering a secure and convenient way to store and process sensitive information.

Why Card Features and Elements Matters?

Card features and elements matter because they are the foundation of secure and efficient financial transactions. The intricate design of card features and elements, including the card number, expiration date, CVV, and chip technology, is essential for verifying the card’s authenticity and ensuring the safety of the cardholder’s funds and personal information. These features act as a robust security mechanism, deterring unauthorized access and usage and thereby protecting the integrity of each transaction.

The importance of card features extends to facilitating seamless transactions for consumers and merchants. The efficiency of magnetic stripes, EMV chips, and contactless payment technology streamlines the payment process, reducing transaction times and enhancing the overall user experience. Efficiency is vital in today’s fast-paced commerce environment, where speed and convenience are highly valued. Standardizing card features ensures compatibility across different payment systems and devices, broadening the scope of their usability and fostering a more inclusive financial ecosystem.

Card features play a pivotal role in fraud prevention. The unique combination of card details creates a formidable barrier against fraudulent activities. EMV chip technology, in particular, is instrumental in combating fraud by generating a unique transaction code for each payment, making it extremely difficult for fraudsters to replicate or clone the card. These security measures collectively contribute to significantly reducing card-related fraud, safeguarding consumers and merchants from potential financial losses and reputational harm.

Contactless payment technology has further enhanced the security and convenience of card transactions. Contactless payments allow quicker and more secure transactions by utilizing Near Field Communication (NFC), as they eliminate the need for physical contact with the payment terminal, thereby reducing the risk of card skimming and other forms of theft. The widespread adoption of contactless payments underscores the importance of advanced card features in today’s payment landscape.

What are the Major Cards Accepted in Most Transactions Around the World?

The major cards accepted in most transactions around the world are listed below.

- Visa: Visa is an eminent global payment technology corporation facilitating electronic fund transfers across its extensive network. The first 4 digits of Visa cards invariably commence with the number 4, serving as their identity marker. Visa cards typically boast 16 digits, offering various options, including credit, debit, and prepaid variants, and are ubiquitously accepted worldwide. Distinctive elements encompass the Visa emblem, a holographic dove, a chip for secure transactions, and a magnetic stripe, rendering them easily identifiable.

- Mastercard: MasterCard is a renowned multinational financial services conglomerate that provides various payment processing products and services. The MasterCard first 4 digits, sometimes known as MasterCard first 4 numbers, usually start with the number 5, with the second digit ranging between 1 and 5, distinguishing them in the financial realm. These cards generally contain 16 digits and are accepted in many countries, offering credit, debit, and prepaid solutions. Key distinguishable features include the MasterCard logo, which comprises two intersecting circles in red and yellow, in addition to a chip and a magnetic stripe.

- Discover: Discover stands as a distinguished financial services entity renowned for its credit card offerings and the operation of the Discover Network for payment processing. The first 4 digits of the Discover card typically initiate with the number 6, specifically 6011 or 65, serving as a unique identifier. Discover cards usually possess 16 digits and enjoy widespread acceptance in the United States, providing various rewards and benefits. The Discover logo, an orange and black oval, and a holographic security feature are prominent elements that set these cards apart.

- American Express: American Express, a multinational financial services titan, specializes in premium payment card services and is renowned for its exclusive offerings. American Express cards are characterized by their starting digits, either 34 or 37, marking their distinctiveness in the financial world. American Express cards are lauded for their rewards programs and services, particularly in the travel and business sectors, which typically feature 15 digits. Distinguishable attributes include the Centurion or “Gladiator” logo, a unique card design, a security chip, and a hologram, enhancing their security and recognizability.

How can you Protect your Card?

You can protect your card by being vigilant about where and how you use it. Maintain the integrity of the card by refraining from divulging sensitive information such as the card number, expiration date, or CVV to any third party. Vigilantly scrutinize account statements for unauthorized transactions and promptly notify the card issuer of any discrepancies.

Ascertain the use of secure websites with “https” in the URL and verify the presence of a padlock symbol in the browser during online shopping. Contemplate utilizing a virtual card number for online transactions if the banking institution provides the service, as it offers an additional safeguard. Exercise caution when engaging in transactions over public Wi-Fi networks, as they lack adequate security measures.

Preserving the physical card and safeguarding online card data is of paramount importance. Employ robust and distinct passwords for online accounts associated with the card, and consider leveraging a password manager for enhanced security. Implement two-factor authentication (2FA) wherever required to fortify the defense against unauthorized access.

Remain vigilant of the surroundings when utilizing a card in public venues. Conceal the keypad while inputting the PIN at ATMs or point-of-sale terminals to avert the risk of shoulder surfing. Opt for an RFID-blocking wallet or sleeve to thwart unauthorized scanning of contactless payments. One mitigates the risk of card fraud and ensures the card’s and financial data’s security by adhering to these measures.

What are the Benefits of Card Features and Security Elements?

The benefits of card features and security elements are listed below.

- Fraud Mitigation: Advanced security measures such as EMV chips and tokenization significantly diminish unauthorized transactions. Advanced security measures make replicating or counterfeit cards more challenging for malefactors.

- Augmented Security: Biometric authentication, such as fingerprint recognition, and the utilization of one-time passwords (OTPs) provide an additional layer of security. These features ensure that only the legitimate user accesses and utilizes the card.

- Expediency: Contactless payment technology facilitates swift and effortless transactions, enhancing the consumer experience. It enables more rapid checkout times and reduces the necessity for physical interaction with payment terminals.

- Online Protection: Using virtual card numbers and dynamic CVVs helps safeguard users’ actual card details during online transactions. It reduces the risk of data breaches and unauthorized online purchases.

- Control and Monitoring: Cardholders benefit from real-time transaction alerts, spending limits, and the ability to freeze or unfreeze their card. These features help them monitor and control spending and quickly respond to suspicious activity.

What are the Challenges of Card Features and Security Elements?

The challenges of card features and security elements are listed below.

- Implementation Complexity: Integrating advanced security features such as biometric authentication and EMV chips requires sophisticated technology and infrastructure. It is challenging and costly for financial institutions and merchants to implement.

- User Adoption: Some cardholders resist adopting new security features due to concerns about privacy or the perceived inconvenience of adapting to new technologies. Overcoming the resistance requires effective communication and education to demonstrate the benefits of enhanced security.

- Compatibility Issues: Ensuring compatibility between card features and security elements across various payment systems and devices is challenging. It requires coordination among card issuers, payment networks, and merchants to maintain seamless transaction processes.

- Balancing Security and Convenience: Striking the right balance between robust security measures and user convenience is a significant challenge. Overly complex security protocols deter users, while overly simplified measures compromise security.

- Evolving Threats: The methods employed by fraudsters evolve as technology advances. Keeping pace with evolving threats and continuously updating security features to avoid potential vulnerabilities is an ongoing challenge for card issuers and security experts.

How Amplify Ensure Secure Giving?

Amplify ensures secure giving by employing robust security procedures and processes to protect donor data and transactions. The platform uses encryption technology to protect sensitive data, such as credit card information, during transmission and storage. Amplify guarantees that contributors’ personal and financial information remains secret and protected from illegal access.

Amplify uses secure payment gateways and processors that meet industry standards, such as PCI DSS. Amplify guarantees that all transactions are completed safely and effectively, lowering the likelihood of fraud and data breaches.

Amplify provides features such as two-factor authentication and secure login methods to improve security. These safeguards prevent illegal access to donor accounts and guarantee that only authorized users conduct transactions.

Amplify continuously reviews and improves its security processes to keep ahead of new threats. The platform performs security audits and assessments to detect and resolve vulnerabilities, allowing donors to donate with confidence and peace of mind.

Amplify prioritizes security and implements these procedures to create a safe and secure platform for contributors to support their favorite causes without fear of their personal and financial information being compromised.

How to do a Basic Swipe for your Card?

To do a basic swipe for your card, follow the steps below.

- Prepare the Transaction Terminal: Ensure that the transaction terminal is powered on and ready to accept payments. Locate the card reader slot on the terminal where one performs the basic card swipe.

- Position the Credit Card: Retrieve the credit card and hold it firmly between the thumb and index finger. Orient the card so that the magnetic stripe, containing encoded data, faces downwards.

- Execute the Swipe: Glide the magnetic stripe of the credit card along the designated area of the card reader with a smooth and controlled motion. The action initiates the transfer of encoded information to the terminal, facilitating the transaction.

- Wait for Authorization: Await authorization from the transaction terminal after completing the basic card swipe. The system verifies the authenticity of the card and the availability of funds for the intended transaction.

- Finalize the Transaction: Follow the prompts on the transaction terminal screen to finalize the transaction once authorization is obtained. One is required to confirm the amount and provide additional verification, such as a PIN or signature, depending on the security measures in place.

How to Use My Card for Tithing?

To do a basic swipe for your card, follow the steps below.

- Access the Online Giving App on One’s Device: Open the app on one’s smartphone, tablet, or computer by tapping or clicking on its icon. Ensure one has a stable internet connection for a smooth transaction process.

- Navigate to the Section for Tithing or Donations: Locate the specific section within the app that is designated for tithing or making donations. The section is often labeled clearly for easy access.

- Select the Amount One Wishes to Tithe: Choose the amount one wants to give from the options provided in the app. Some apps also allow one to enter a custom amount if the predefined options do not suit one’s preference.

- Enter the Card Details to Complete the Transaction Securely: Input one’s card number, expiration date, CVV code, and any other required information. Ensure that the app is secure and trustworthy before entering sensitive financial information.

Confirm the Payment to Finalize One’s Tithing Contribution: Review the details of one’s transaction, including the amount and recipient, before confirming the payment in the online giving app. The app must provide a confirmation message or receipt for one’s records once confirmed.